Operational Finance : Finance for Managers, Certification link.

1. Financial Analysis

- Operational Finance focuses on the daily activities driving a business forward.

- a model of financial analysis and diagnosis, using financial forecasts, and designing an action plan when needed.

- Corporate (or Structural) Finance : studies how to finance the fixed assets, and also the combination of debt and equity that a company should have.

- Strategic Finance: focus on developing comprehensive financial plans for their companies

Case Study : Ask credit from a bank (Credit (short term) and Loan (long term)).

1.1 Business Analysis

What are you doing? Business analysis to build expectation.

- Sales:

- What? Where? Economic condition.

- Cyclicality - fit with the economic cycle (e.g. car industry).

- Seasonality (e.g. ice-cream).

- Clients / Suppliers.

- Strategy (why am I good to my clients?): cheap, good, variety.

- Management team - trust.

1.2 P&L Analysis

Do you make money?

- Sales: value and growth. Growth could be large for startup.

- Gross Margin & COGS (costs of good sold) : percentage of sales.

- OPEX (operational expense) : electricity, salaries, overhead.

- Operating profit / Sales.

- EBITDA / Sales.

- Financial Results (~2.5% EBIT).

Operational Risks vs. Financial Risks (interest expenses with stable income).

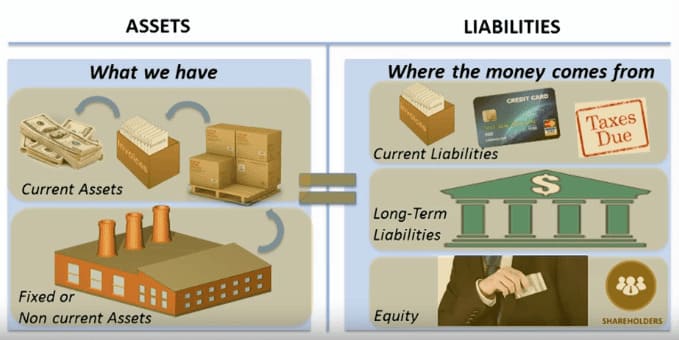

1.3 Balance Sheet Analysis

Do you need money?

- Look at the big numbers.

- Look at the evolution over the years.

- Look at the operational ratios.

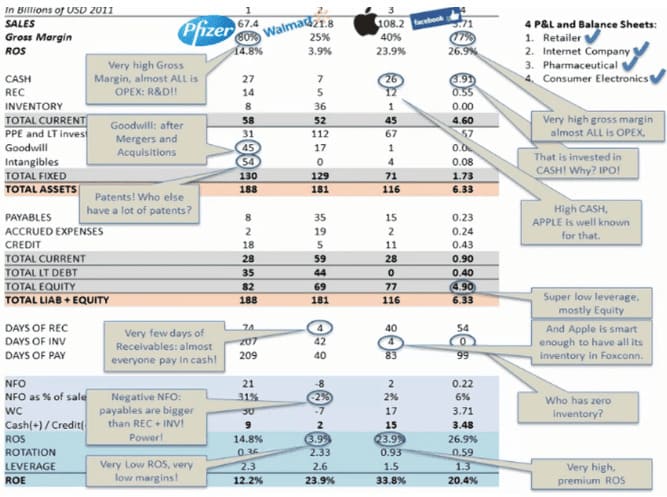

2. Operational Ratios and Forecasting

2.1 Operational ratios

Days of Collection: (for receivables) the number of days the customers take to pay.

- $Days\ of\ Collection = \frac{RECEIVABLES}{Daily\ Sales}$ (“Daily Sales” is sales per day)

- Impact (of customer pay delay): $Extra\ Money\ Needed = Days\ Delay * Daily\ Sales$

Days of Inventory: the number of days I take to sell the inventory.

- $Days\ of\ Inventory = \frac{INVENTORY}{Daily\ COGS}$

- Impact (of excess inventory) : $Extra\ Money\ Needed = Days\ More * Daily\ COGS$

- “Turns Over” = inverse of “Days of Inventory”

Days of Payment (to suppliers) : the number of days I take to pay the suppliers.

- $Days\ of\ Payment = \frac{PAYABLE}{Daily\ PURCHASES}$

- $Stock\ Initial + Purchases - COGS = Final\ Stock$, $Purchases \approx COGS$

- Impact: $Extra\ Money\ Free = Days\ Delay * Daily\ PURCHASES$

Takeaways:

- The evolution tell if the company is well managed.

- look at the consequences in the balance sheet: longer collection, inventory or payment.

- top management usually believes that the condition (collection, inventory, payment) is better than it really is.

2.2 Forecast

Forecast P&L - Forecast Sales, then others.

Forecast Balance Sheet, derived from sales. Put cash and credit at the end. If total assets > (total liabilities + equity) , the difference will go to credit.

3. Diagnosis and Action Plan

3.1 Diagnosis

Diagnosis: Why do they need more and more credit? Structure problem : as company grow, the need of funds to operate grows faster than the working capital.

Need of Funds (NFOs) are funds required to finance a company's operations.

- Sources of needness for money : Delay in selling what you buy from suppliers - receivables and inventory.

- NFO = RECEIVABLES + INVENTORY - PAYABLES (directly related to sales)

- NFOs are "use of assets".

Working Capital (WC) is the long-term funding available to finance the NFO once the fixed assets have been financed.

- WC = EQUITY + LONG-TERM DEBT - FIXED ASSETS or WC = Current Assets - Current Liabilities

- WC is "source of funds".

- if NFO < WC, we have extra CASH.

- id NFO > WC, we need to ask for CREDIT.

3.2 Action Plan

Plan to solve the problem drawn from diagnosis.

- NFO : Changing REC, INV, PAY.

- WC: Changing LT Debt, FA, or Equity. We could work on P&L (making money).

Sustainable Growth : WC should grow faster or equal to NFO. $\Delta NFO <= \Delta WC$

- $\Delta NFO_{t} = NFO_{t}^{\%} * \Delta Sales_{t}$ (assuming NFO per sale is constant)

- $\Delta WC_{t} = \frac{Net\ Income_{t}}{Sales_{t}} * Sales_{t} = ROS_{t} * (Sales_{t -1} + \Delta Sales_{t})$ (with Return on Sales,ROS)

- As a result , $\frac{NFO_{t}^{\%} * \Delta Sales_{t}}{Sales_{t -1}} = \frac{ROS_{t} * (Sales_{t -1} + \Delta Sales_{t})}{Sales_{t -1}}$

- We have $NFO_{t}^{\%} * g = ROS_{t} * (1 +g)$

- We have $g = \frac{ROS_{t}}{NFO_{t}^{\%} - ROS_{t}}$

4. Sensitivity Analysis, NFO Revisited, and ROE

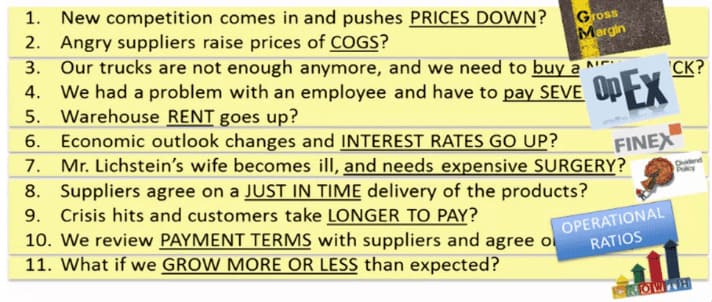

Sensitivity Analysis, how sensitive the results are if the key variables changed.

Seasonal Companies

Return On Equity ROE, more interesting for shareholders.

\[ROS = \frac{Net\ Income}{Salse} \frac{Sales}{Assets} \frac{Assets}{Equity} = ROS * Turnover * Leverage = \frac{Net\ Income}{Equity}\]Blind Financial Statements