Options

The benefits of options:

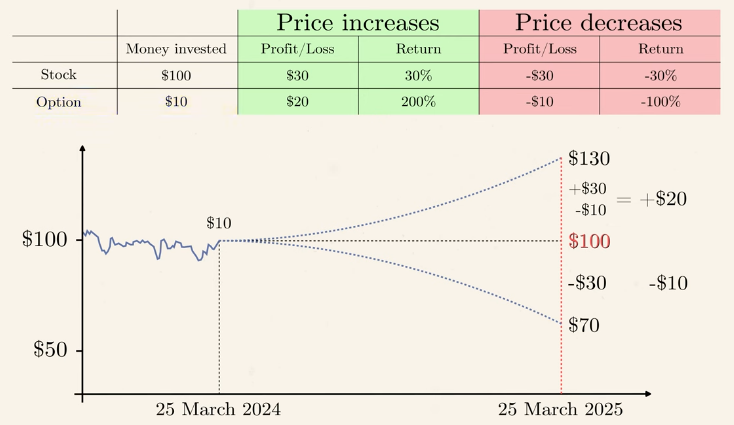

- Limit your downside (loss is relatively smaller).

- Provide leverage (return - ratio is much larger).

- Use as a hedge (to reduce risk).

Random

The Radiation of Probabilities. Stock price follows a random walk - Galton Board - Brownian motion.

- a collection of random work creates the normal distribution.

- same as heat radiates from regions of high temperature to regions of low temperature.

Bacelier - based on this random model. Price of an option - equalize the profit and loss.

Earn Money

Thorpe. (Card counting in blackjack) made a risk-free portfolio of options.

- Dynamic Hedging. $\Pi = V - \Delta S$

- Take the draft (

momentum in the stock price ) into account.- cheap -> buy

- overvalued -> short sell

The pricing of options and corporate liabilities 1973 Black, F., & Scholes, M. publish the idea. should not exist a risk-free portfolio.

- Change in price = drift + randomness : $dS = Sdt + \delta S dz$

- Black-Scholes/Merton Equation : $\frac{\partial V}{\partial t} + rS \frac{\partial V}{\partial S} + \frac{1}{2} \delta^{2} S^{2} \frac{\partial^{2}V}{\partial S^{2}} - rV = 0$

- Following the function, we have explicit expression of $C = N(d_{1}) S_{t} - N(d_{2})K e^{-rt}$.

- Chicago Borad Options Exchange (CBOE) founded.

Renaissance - Medallion fund.

- Challenge to the hypothesis of market efficiency.

- There exist patterns in stock market.